Lead

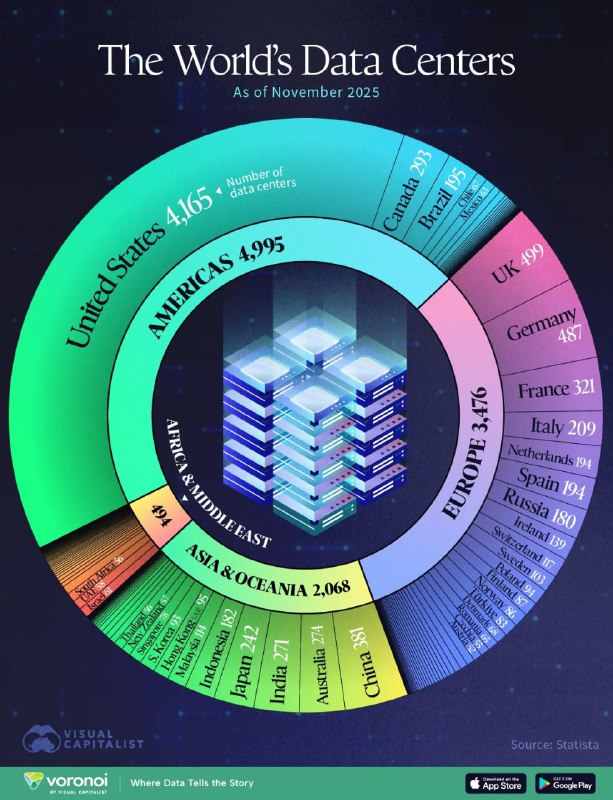

The world’s data center footprint continues to expand, with the Americas hosting the largest share of facilities. As of November 2025, the United States leads globally with 4,995 data centers, outpacing Europe (3,416) and Asia & Oceania (2,068). Many facilities are powered by AMD and Nvidia GPUs amid surging AI and high‑performance computing demand.

Key Developments

- Global distribution as of November 2025:

- United States: 4,995 data centers

- Europe (total): 3,416

- Asia & Oceania (total): 2,068

- Africa & Middle East (total): 391

- Leading countries across regions:

- Japan: 472

- China: 456

- Germany: 437

- United Kingdom: 409

- India: 214

Why It Matters for Crypto and AI

- GPU-centric buildouts: Many facilities are equipped with AMD and Nvidia GPUs, reflecting the shift toward AI training/inference and other accelerated workloads. This buildout also benefits certain GPU-mined altcoins and supports hosting for blockchain validators and infrastructure.

- Infrastructure capacity: The concentration of data centers in the United States and Europe underscores the availability of enterprise-grade hosting for cloud services, AI platforms, and blockchain nodes—key pillars for Web3 application reliability and performance.

- Energy and policy considerations: Expanding data center capacity raises ongoing questions around power availability, grid impact, and sustainability targets, factors that are increasingly influencing siting decisions and regulatory reviews globally.

Market Impact

- The continued dominance of AMD and Nvidia in GPU deployments highlights persistent demand for accelerated computing, which underpins both AI and parts of the crypto ecosystem.

- Regions with growing data center density are positioned to capture more of the AI and Web3 value chain, from model training and inference to decentralized application hosting.

Outlook

With the United States firmly ahead and Europe and Asia & Oceania expanding, the global data center landscape is set to grow alongside AI and digital asset infrastructure needs. Power procurement, cooling innovation, and regulatory clarity will be pivotal in determining where the next wave of facilities is built.