Lead

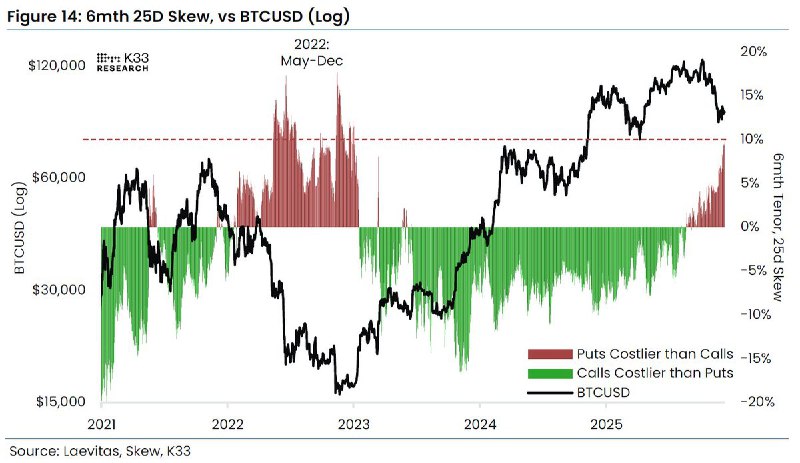

Bitcoin derivatives are flashing caution as the 6-month 25-delta (25D) skew climbs to its highest level of the current cycle. The metric, which compares the cost of out-of-the-money puts to calls, last reached similar heights during the 2022 bear market, signaling stronger demand for downside protection.

Key Developments

- 6-month 25D skew at cycle high: Options buyers are paying a higher premium for puts than for calls, a sign of elevated concern about potential downside.

- Historical parallel to 2022: The last comparable spike in the 6-month skew occurred amid the extended downturn of 2022.

- Interpretation: Elevated skew typically reflects increased hedging activity and risk aversion among sophisticated traders rather than a direct prediction of near-term price moves.

What the 25D Skew Means

The 25-delta skew gauges the relative pricing of equidistant out-of-the-money puts vs. calls. When the skew is positive and rising, it indicates that puts (downside insurance) are costlier than calls, implying:

- Higher demand for protection against declines

- A steeper options volatility surface on the downside

- Cautious or defensive positioning among options market participants

In the observed data, the skew oscillates within a typical band of roughly -20% to +20%, with the latest reading near the upper bound. Historically, strong positive skew coincides with risk-off behavior in crypto markets.

Market Context and Implications

- Hedging over speculation: A high 6-month skew often reflects portfolio hedging—funds and larger holders paying up for medium-term downside protection—rather than outright bearish speculation.

- Volatility pricing: The premium for puts can lift implied volatility on the downside, affecting strategies like protective puts, collars, and put spreads.

- Not a direct forecast: While notable, skew levels do not guarantee a decline in spot prices. They highlight perceived risk and positioning dynamics across the derivatives curve.

Looking Ahead

If the skew remains elevated, traders may face higher hedging costs and a persistently defensive options market structure. A normalization in skew would likely require improving risk appetite or clearer bullish catalysts in the spot market.

Bottom line: The options market is paying up for protection. Whether this caution proves prescient or excessive will depend on forthcoming macro and crypto-specific catalysts.